By

By

In late May, OPEC (Organization of the Petroleum Exporting Countries) and non-OPEC oil producers agreed to extend production cuts through April 2018 in the face of oil inventories that remain well above average. While one would have expected a positive market reaction, many investors believed deeper cuts were necessary and the market has sold off sharply since the meeting. The selloff indicates that many investors are no longer relying on OPEC to balance the oil market as concerns about high US inventories and growing US production persist.

Why are investors so dismissive? Why haven’t US inventories budged? I see three reasons for this:

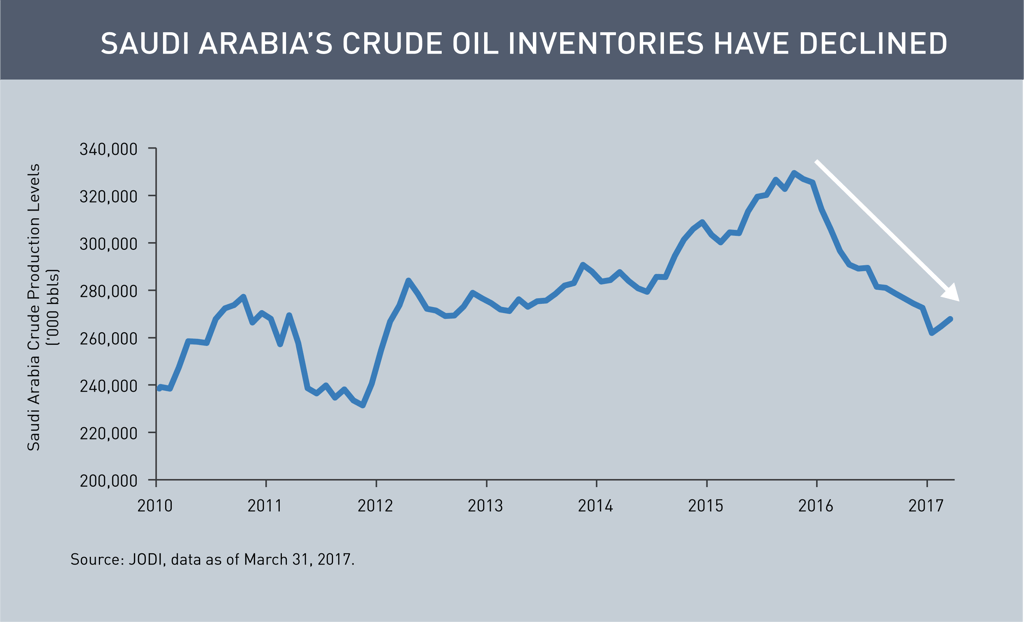

1. OPEC oil exports remained steady as OPEC drew on inventory

OPEC nations followed the letter of the law on production cuts, but they drew on existing inventories in the first quarter, leaving oil exports little-changed through much of the period. But with exports down significantly over the past month, the US, Europe and other markets should start to feel the impact of the OPEC cuts on their inventories.

Additionally, investors know that Saudi Arabia decreases exports during the summer as higher cooling demand drives domestic oil consumption. US inventories should fall as a result.

2. OPEC’s ability to control prices appears to have waned…

The market has largely lost faith in OPEC’s ability to control oil prices. US oil production rebounded after OPEC announced cuts last fall, and many believe shale is the new swing producer, eliminating the need for OPEC spare capacity to meet supply disruptions. However, shale is highly capital intensive and typically cannot respond to significant short-term supply disruptions. It's no secret that OPEC would like to normalize oil inventories in order to regain control of prices through the utilization and restraint of spare capacity. It appears OPEC hopes to drive the near-term price of oil higher than the long-term price by reducing the large inventory overhang. A lower long-term price should discourage additional investment in shale.

3. ...because of OPEC’s past missteps

One of OPEC’s major follies during the boom years in 2009-2014 was claiming oil prices at $100 per barrel were “fair.” At those prices, oil companies went on wild spending sprees, sanctioning numerous projects that depended on oil prices at $70-80 per barrel or higher to break even. Ironically, this led to US shale production exploding as infrastructure expanded supported by massive investment in exploration and innovation. In hindsight, it appears that OPEC should have increased production when outages such as the ones in Kazakhstan and Libya occurred, but instead it allowed shale and expensive production to fill the gap. Of course, hindsight is 20/20 and OPEC is now trying to correct its past missteps by normalizing inventories in an attempt to regain pricing power.So, has OPEC lost its touch? Is OPEC irrelevant?

OPEC lost a lot of its clout during the downturn in oil prices. Many bullish and long-term investors have lowered their expectations over the past several months due to growing shale production and OPEC’s inability to quickly fix the oversupplied market. However, the extended cuts should lead to a more balanced market over the next year. I believe OPEC’s relevance will emerge in the next few months as inventories diminish, and the cartel can still exert considerable influence on oil prices and fundamentals.

Past performance is no guarantee of, and not necessarily indicative of, future results.

Commodity interest and derivative trading involves substantial risk of loss.

This is not an offer of, or a solicitation of an offer for, any investment strategy or product. Any investment that has the possibility for profits also has the possibility of losses.

MALR018904

Market conditions are extremely fluid and change frequently.

This blog post is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the

subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Information, including

that obtained from outside sources, is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or

redistributed without authorization. This information is subject to change at any time without notice.