By

By

We believe the municipal bond market is on the brink of major changes. The Biden administration has proposed legislation that, if passed, could meaningfully increase both taxable and tax-exempt supply in the municipal bond market. While this potential shift could cause some short-term disruption, we believe it could result in more balanced supply and demand over the medium term.

Revisiting Trump’s Tax Cuts and Jobs Act

To explain the impact of the proposed changes, we need to revisit how the Tax Cuts and Jobs Act (TCJA) of 2017 affected the municipal bond market. In our view, the TCJA significantly changed supply and demand in the municipal market in three key ways:

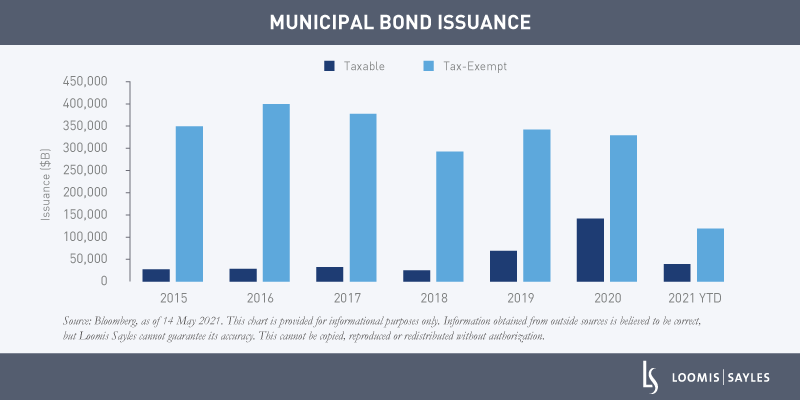

- Tax-exempt issuance fell sharply because the TCJA prohibited advance refunding of tax-exempt debt with tax-exempt issuance.

- Taxable issuance rose more than four-fold as supply shifted from the tax-exempt market to the taxable market.

- The State and Local Tax (SALT) deduction limitation fueled demand from individual investors in high-tax states.

Aside from the March panic last year, these conditions have provided a consistent market backdrop for more than three years. The TCJA increased supply in the taxable municipal market, giving non-traditional municipal buyers more access to a higher-quality, higher-yielding, predominantly longer-duration alternative to corporate credit. But it simultaneously starved traditional municipal investors in the tax-exempt market of sufficient paper to meet increased demand. As a consequence, municipal bonds have reached record-high valuations versus US Treasurys.[i] In fact, valuations have become one of the largest factors restraining yields from moving even lower.

These conditions are likely to change under the Biden administration, though we won’t know when and how until legislation passes. Below, we take a closer look at potential changes that we believe would have a significant impact on the municipal bond market.

Restoration of tax-exempt advance refunding

(High probability)

In our view, permitting state and local governments to use tax-exempt issuance to advance refund higher-rate debt would migrate nearly all tax-exempt refunding issuance from the taxable market back to the tax-exempt market. This could amount to a $100 billion shift in supply in our opinion. To put this in perspective, tax-exempt issuance last year was $329 billion and taxable issuance was $146 billion.[ii] Bipartisan support of this move increases its odds of passing later this year.

Instituting a taxable municipal bond subsidy program (similar to Build America Bonds) to finance infrastructure investment

(Strong probability)

The taxable municipal market could potentially replace lost supply from a refunding shift with an even larger source of issuance if Congress passes infrastructure legislation. Current administration officials are keen backers of taxable subsidy bonds—bonds with interest rates subsidized by the federal government, which lowers the cost of borrowing for state and local government infrastructure projects. If an infrastructure package passes, a substantial portion of the financing would likely come in the form of taxable municipal bonds.

To gauge the potential magnitude of this issuance, consider that the proposed $2.3 trillion infrastructure plan calls for nearly $1 trillion of capital investment to fund transportation, clean water, power and broadband access. Compare that to the Build America Bond (BAB) program, a small component of the roughly $800 billion American Recovery and Reinvestment Act. BAB issuance amounted to $181 billion from 2009 to 2010.[iii] That means the size of the Biden administration’s proposal could potentially amount to several hundred billion in taxable municipal issuance over the next few years.

Increasing or eliminating the SALT deduction limitation

(Increase more likely than elimination)

Increasing or eliminating the state and local tax (SALT) deduction limit has gained some traction lately. Legislators from high-tax states have championed the issue, but the administration has not yet weighed in on the SALT cap. Barclays has estimated that eliminating the cap would cost nearly $700 billion over a ten-year window, and this cost is likely to be a factor in Congress.[iv] If the SALT cap is altered, we would expect it to dampen the demand for tax-exempt issuance overall and particularly for so-called “specialty state” paper (bonds issued in high-tax states exempt from state income tax).

Dramatic changes could result in a better-functioning market

We think upcoming legislation is very likely to alter the supply/demand dynamic in the municipal bond market over the medium term. While supply and demand shifts could result in short-term valuation adjustments, we believe they would create a better-functioning market and help provide active investors with more relative value opportunities over time.

[i] Source: Bloomberg, as of 17 May 2021.

[ii] Source: The Bond Buyer.

[iii] Source: US Treasury.

[iv] Barclays, “US Public Policy, Economics, & Municipals: President’s Two-Part Stimulus and Tax Plan Takes Shape,” published 29 April 2021.

MALR027305

There is no assurance that developments will transpire as forecasted and actual results will be different. Information, including that obtained from outside sources, is believed to be correct, but Loomis Sayles cannot guarantee its accuracy.

Market conditions are extremely fluid and change frequently.

Market conditions are extremely fluid and change frequently.

This blog post is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the

subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Information, including

that obtained from outside sources, is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or

redistributed without authorization. This information is subject to change at any time without notice.