By

By

By Celeste Tay, Senior Sovereign Analyst and Kaimin Khaw, Sovereign Analyst

For years, President Trump has accused China of purposely devaluing the renminbi to boost exports. With trade and political tensions boiling over, the question of whether China will devalue the renminbi often comes up. We don’t think China will intentionally weaken the renminbi to counteract US tariffs. Yes, it weakened about 2.5% versus the US dollar in May when trade tensions resurfaced, but the weakness was largely market-driven. Chinese authorities have, in fact, leaned hard against renminbi depreciation through verbal intervention and tightening capital controls on residents. Evidence also suggests Chinese authorities have unofficially redeployed the counter-cyclical adjustment factor to fix the renminbi at stronger levels.[i]

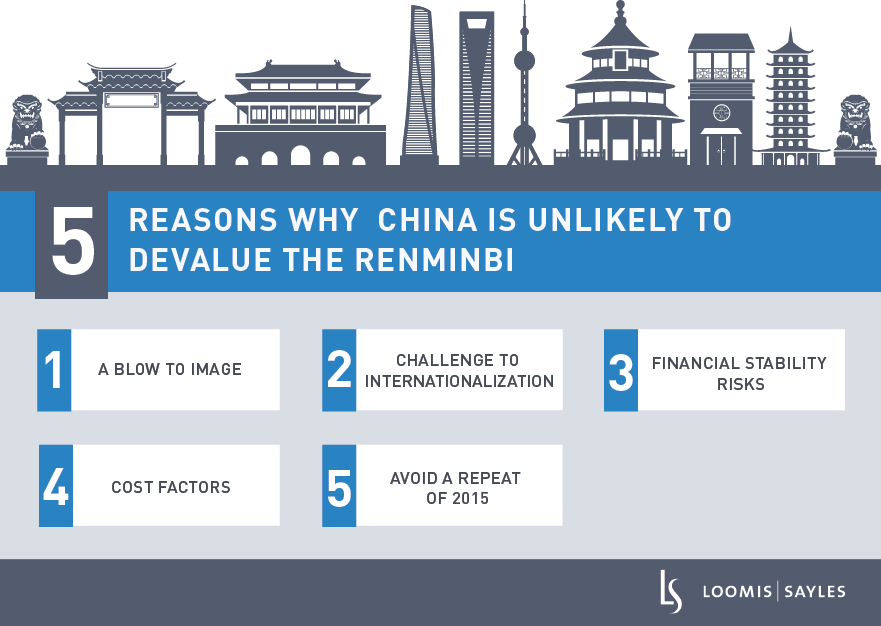

Big picture, the costs of a weaker currency can outweigh the benefits for China. Here are five reasons why:

- A blow to image. China wants to position itself as a defender of free trade to promote dialogue with non-US partners.

- A challenge to renminbi internationalization. China has been working hard to raise the natural global demand for the renminbi. Depreciation would dampen interest in holding the currency.

- Financial stability risks. A weaker renminbi inflates external debt costs and raises worries over the health of China’s financial system.

- Cost factors. A weak renminbi makes imported goods more expensive for Chinese consumers. It also raises the costs of imported inputs for Chinese exports, limiting the potential boost to exports.

- Avoid a repeat of 2015. A wave of capital poured out of China in 2015 after so-called “renminbi devaluation.” China used roughly $1 trillion in foreign currency reserves to stabilize the renminbi and restore investor confidence. Authorities do not want another costly confidence rout.

[i] The renminbi remains a managed currency. The People’s Bank of China fixes the US dollar-Chinese yuan (USDCNY) central parity rate based on: 1) the previous day’s close, and; 2) movements of the US dollar against a basket of currencies. The USDCNY rate is only allowed to fluctuate within +/- 2% of the central parity rate. Estimated model errors have been showing up persistently and meaningfully negative, suggesting that the People’s Bank of China has been fixing the USDCNY rate at levels weaker than implied by this formula (i.e., a stronger renminbi).

MALR023717

Market conditions are extremely fluid and change frequently.

This blog post is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the

subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Information, including

that obtained from outside sources, is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or

redistributed without authorization. This information is subject to change at any time without notice.